By Annik Forristal, Kailey Sutton, Laura Brazil and Geza Banfai

Special to Ontario Construction News

Indemnities and limitations of liability are key contractual risk allocation provisions found in most construction contracts.

Unfortunately, they can also be complicated and difficult to understand, and contractors sometimes gloss over them. This is a mistake. Indemnity clauses in particular can contain some unexpected risks for the contractor, and it is essential that these be understood before signing.

In this article we consider the fundamental components of these contract clauses and how they allocate risk, with a focus on what contractors should look out for when reviewing them.

Indemnity clauses

Legally, an indemnity is simply a contractual promise to cover a loss. One party (the “indemnifier”) promises to “indemnify” (i.e., “make whole”, “compensate” or “protect against liability”) the other party (the “indemnitee”) against the harm or loss which the clause stipulates.

One might ask why an indemnity is necessary at all – would not an ordinary claim for breach of contract and/or negligence be sufficient to protect the innocent party? The answer is: not necessarily. There are losses which may not otherwise be recoverable under the contract or in claims for negligence, and the indemnity fills in those gaps. In some circumstances, pursuing an indemnity claim may also be procedurally easier and less cumbersome than proving a breach of contract or negligence.

To illustrate, compare a warranty clause with an indemnity. Under a warranty, the contractor promises to replace or re-perform – but not all losses due to defective work are necessarily curable by replacement or re-performance (e.g., business losses due to downtime while the warranty repair is performed). Depending on its wording, an indemnity clause can offer protection against those losses too.

A contractor agreeing to indemnify must therefore recognize that its exposure to loss may be increased.

The key considerations for the contractor are:

- How much increased exposure is reasonable in the circumstances;

- Are any of these risks insurable; and

- How much added uninsured risk is the contractor prepared to

The following is an example of the indemnity provision in the standard form CCDC 2 2020 – Stipulated Price Contract document:

13.1.1 Without restricting the parties’ obligation to indemnify respecting toxic and hazardous substances, patent fees and defect in title claims all as described in paragraphs 13.1.4 and 13.1.5, the Owner and the Contractor shall each indemnify and hold harmless the other from and against all claims, demands, losses, costs, damages, actions, suits, or proceedings whether in respect to losses suffered by them or in respect to claims by third parties that arise out of, or are attributable in any respect to their involvement as parties to this Contract, provided such claims are:

Generally speaking, an indemnity provision can be broken into three main parts: (1) who is providing the indemnity and who is benefitting from it, (2) what is covered by the indemnity, and (3) how is that indemnity triggered. When reviewing any indemnity clause it is useful to separately consider each of these three parts to understand how the clause allocates risk between the parties.

Who is providing the indemnity? Who is benefitting from it?

In any indemnity clause the person providing the indemnity (the “indemnifier)”) and the person(s) benefitting from the indemnity (the “indemnitees”) should be clearly identified. For example, the CCDC 2 indemnity is mutual, with each party providing the other with an indemnity:

Indemnifier: Contractor Indemnitee: Owner

AND

Indemnifier: Owner Indemnitee: Contractor

It is possible to vary this. For example, an indemnity can be one-sided, flowing only one way:

Indemnifier: Contractor Indemnitee: Owner

An indemnity clause can also include additional benefitting parties (such as directors, officers, agents, affiliates, lenders, landlords and so on):

Indemnifiers: Contractor Indemnitees: Owner and its affiliates, directors, officers, employees and agents

The CCDC 2 indemnity is a mutual indemnity between the Contractor and the Owner – no other parties are indemnitees entitled to benefit from the protection against loss and liability. But, for example, when the Owner is a tenant of the property, the landlord may also suffer losses if the Contractor is negligent, and the landlord’s consent to the tenant improvement may be conditional upon appropriate protections for the landlord in that event. For this reason, such an Owner may require an amendment to the CCDC 2 indemnity through supplementary conditions to include its landlord as an indemnitee:

Indemnifier: Contractor Indemnitee: Owner and Landlord

AND

Indemnifier: Owner Indemnitee: Contractor

It is necessary for the contractor to consider on a case-by-case basis whether anyone identified as an additional indemnitee is appropriate. Helpful questions to contemplate include: Do we know who this person is? What is the likelihood of this person suffering a loss? What level of control or involvement does this person have in the subject matter of the contract?

What does the indemnity cover?

A prudent contractor should be acutely aware of what types of claims or losses are covered by the indemnity provision they are being asked to sign.

An indemnity can be – and many are – wide open and not limited in any way. They typically contain language like this:

“The contractor shall indemnify the owner for any and all losses, of every nature and kind, whether in contract, tort or under any other legal theory…”.

The problem with an indemnity like this is that it puts the contractor at risk to cover an undefined and unquantified range of losses, many of which the contractor can neither anticipate nor manage. Even a relatively trivial failure to perform can expose the contractor to the loss of its entire profit on the contract, or worse.

As examples, indemnity clauses may expressly cover liability for legal fees and consequential damages, both of which are types of loss that can be substantial in quantum and escalate quickly. They may also require the contractor to “defend” and/or “protect” the indemnitee. This obligation to “defend” or “protect” can go further than simply indemnifying for losses, and require the contractor to provide a legal defense in any lawsuit in which the indemnitee is named, whether or not the contractor is at fault, and whether or not the lawsuit has any merit. Compounding the problem is that these legal defense costs may not be covered by policies of insurance.

These issues are closely related to how an indemnity is triggered and limitations of liability clauses, which are covered below.

How is the indemnity triggered?

When reviewing any indemnity clause, it is also important to consider when the obligation to indemnify is triggered, i.e. what needs to happen for the indemnifier to be liable.

The most common triggers for liability under an indemnity are the indemnifier’s negligence or breach of contract. This is the case under the CCDC 2 indemnity, and represents one industry standard. To recover under the indemnity, the indemnitee must show either negligence by the contractor or a breach by the contractor of some contractual obligation.

Some indemnity clauses, however, include triggers that are much broader, such as:

“any losses suffered due to performance of the work”.

Liability under such an indemnity can potentially be triggered https://accisotret.com solely by performance of the work, even if it was performed well and in accordance with the contract. Broad triggers like this can significantly increase the indemnifier’s risk by exposing it to liability for losses that are less likely to be covered by its insurance and beyond what it would otherwise be responsible for at law.

When reviewing an indemnity clause, the contractor should therefore consider the content of the indemnity (what it covers and how it is triggered) to confirm that it is appropriate for the scope and project.

Questions to ask include:

- What are the key risk factors in entering this agreement?

- Is there anything out of the ordinary in terms of this project scope and risks involved, and has this been accounted for?

- Is the risk allocation fair to both parties?

- Is the other party indemnifying for everything it should?

- Are there limits to these risks and are they appropriate?

- To what extent would these losses be covered by insurance?

Contractors should also note that indemnities are not always found in the “indemnities” section of the contract – they may also be found embedded in other provisions. Examples include: confidentiality provisions, which often include an indemnity protecting against losses resulting from a breach of confidentiality; intellectual property provisions, which may include an indemnity providing protection against third party intellectual property claims; and hazardous materials and substances clauses, which again often include an indemnity compensating the innocent party for any losses resulting from such materials. The contractor should be careful to review the whole of the contract to get a full picture of the indemnity risk they are being asked to assume.

The contractor should also consider whether the duration of the obligation to indemnify is reasonable for the circumstances. Indemnity provisions can be subject to limitations in time, substance, and value. For example, the obligations to indemnify set out in the CCDC 2 indemnity are not perpetual – instead, the time limit prescribed by limitations legislation prevails, with an outside time limitation of 6 years. Similarly, contracts will often limit or cap the amount or type of losses for parties are liable. These limitations to indemnity provisions are addressed in the sections below.

Limitations of liability

What is a Limitation of Liability Clause?

Limitation of liability clauses are a common tool permitting the parties to better manage their risk exposure, including exposure under indemnity clauses.

They come in various forms, and for example, may exclude altogether certain types of claims and/or limit the amount which can be recovered. They may be mutual, one-sided, or distinct for each party. Limitation of liability clauses often distinguish between losses covered by insurance and uninsured losses (treating each differently), as well as limiting the types of indemnified claims, and addressing separately claims of third parties. It is also not unusual for these clauses to limit recovery to direct damages only, and waive liability for indirect, special and consequential damages.

Ontario Courts will generally uphold and enforce limitations of liability clauses, especially in the commercial context, unless they are found to be truly unfair or unreasonable. Well-drafted limitations clauses will include clear and unambiguous language and should be prominently placed in the contract instead of buried amongst other provisions.

Why is it important?

At law, there is no assumption that the financial risk or costs associated with a contract will be limited to the price of that contract. To put it starkly: absent any limitation of liability clause, the party’s exposure to liability will be limited only by the other party’s ability to prove responsibility for the loss under some legal theory, and by their ability to prove the quantum of that loss.

Without clear language addressing liability for certain risks, it is possible that the contractor will be subject to excessive and disproportionate losses under the contract. While certain types of claims may have natural thresholds and may therefore be more predictable (e.g., a claim for reimbursement of the costs of discharging a lien), other types of losses can be much more complex and quickly exceed the scale of risk envisioned by the parties (e.g., consequential damages and lost profits). Some of this exposure can be mitigated by insurance (e.g., liability for personal injury or property damage sustained by a third party), but where insurance is either not available or insufficient in amount, the results can be particularly disastrous for the responding party, including potential insolvency.

It is therefore strongly recommended that contractors carefully review draft contracts to identify the potential liabilities to which they are exposed, and seek to limit that exposure by either expressly excluding certain claims that are not appropriate or fair for the contractor to carry, or capping the amounts recoverable.

What to look for:

Any contract that has no limitation of liability clause, or a limitation clause that benefits only the other party, should be a red flag to the contractor. It is strongly recommended that in all cases the contractor seek to include an appropriate limitation clause that is clear and fair. Again, liability under a contract is not tied to the contract’s value – a contractor can expose itself to significant liability just as easily under a $1,000 contract as under a $1 million contract.

When reviewing a limitation of liability clause, parties should consider:their relationship with the other parties to that contract,

- the contract value, and the nature of the services being performed, including their comfort with the subject scope of work,

- the level of risk being undertaken by the contractor and potential third parties who may be

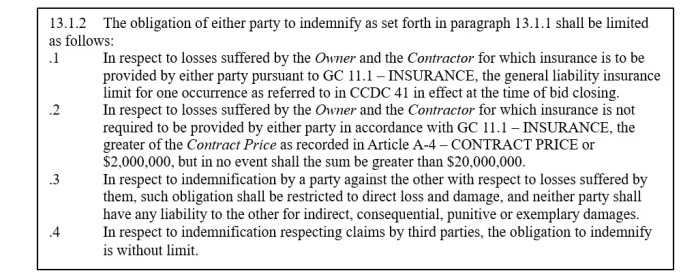

Again, the CCDC 2 2020 – Stipulated Price Contract document provides a good example of an industry standard for a limitation clause:

Notably, this provision:

- Is mutual – it considers “losses suffered by the Owner and the Contractor”;

- Addresses liability for losses covered by insurance, losses not covered by insurance and claims by third parties;

- Provides clear limits – g., “the greater of the Contract Price…or $2,000,000, but in no event shall the sum be greater than $20,000,000”; and

- Excludes liability for consequential, punitive or exemplary damages and limits liability to direct losses: “such obligations shall be restricted to direct loss and damage”.

Note that the CCDC 2 clause does not limit liability for claims by third parties. This is generally considered fair because potential claims by third parties are beyond the control of either party, and this exposure is typically mitigated by insurance which is readily available to the parties.

The writers are lawyers with McMillan LLP’s Construction Group. If you have questions respecting the negotiating, drafting, or implications of the indemnity and limitation of liability provisions in your contract, please reach out to the authors of this article or any member of the practice.

This article is intended as general information only, and does not constitute legal advice. Readers with specific concerns of a legal nature should consult a qualified lawyer.